News

2023 Press releases

P&F Industries, Inc.

Joseph A. Molino, Jr.

Chief Operating Officer

631-694-9800

www.pfina.com

Joseph A. Molino, Jr.

Chief Operating Officer

631-694-9800

www.pfina.com

P&F INDUSTRIES, INC. REPORTS RESULTS FOR THE YEAR ENDED DECEMBER 31, 2022, ANNOUNCES EXTENSION TO BANKING FACILITY

MELVILLE, N.Y., March 28, 2023 - P&F Industries, Inc. (NASDAQ: PFIN) today announced its results from operations for the year ended December 31, 2022. The Company is reporting net revenue of $59,041,000 for the year ended December 31, 2022, compared to $53,554,000, for the same period in 2021. For the year ended December 31, 2022, the Company is reporting a net loss before income taxes of $1,852,000, compared to net income before income taxes of $2,288,000 for the year ended December 31, 2021. The Company noted that during 2021 it recorded as Other Income a gain from the forgiveness of its Paycheck Protection Program loan of $2,929,000 by the Small Business Administration in accordance with the Coronavirus Aid, Relief, and Economic Security Act, known as the CARES Act, and an additional $2,028,000 of Other Income related to the Employee Retention Credits, also provided by the CARES Act. It further pointed out that its full year 2022 loss from operation was $1,482,000, an improvement of $1,115,000, compared to the operating loss of $2,597,000 in 2021.

The Company is reporting a net loss after-tax of $1,476,000, for the year ended December 31, 2022, compared to net income after tax of $2,290,000 for the year ended December 31, 2021. For fiscal year 2022, the Company’s basic and diluted loss per share was $0.46, compared to basic and diluted earnings per share of $0.72 for fiscal 2021.

Richard Horowitz, the Company’s Chairman of the Board, Chief Executive Officer, and President commented, “2022 was a year of transition for P&F. After nearly two years operating under COVID-19 restrictions and conditions, as 2022 progressed, we began to see business begin to show signs of improvement. The transition also was driven by the acquisition of the Jackson Gear Company business in January 2022, which was the primary reason for the revenue growth of just shy of $5.4 million. The largest factor contributing to the $1.1 million reduction in operating loss was the significantly improved Gross Profits at Florida Pneumatic and the tools product lines of Hy-Tech due to both cost reductions and price increases to customers.

Regarding PTG, the acquisition of the Jackson Gear specialty gear business allowed us to penetrate markets we previously were unable to reach and enhanced our position in other markets where we had a modest presence. The integration of this business took longer than expected, but as we enter 2023, PTG is poised for growth as its new order levels continue to increase, has a more modernized facility, and a more established customer base.

As we set our sights on the future, I want to point out that during 2022, our consolidated spending on capital equipment was $2,374,000, with most going into Hy-Tech. Further, we plan on additional capital expenditures of approximately $2.6 million in 2023. I believe that with, new business lines, and modernization of the facilities, P&F, and Hy-Tech in particular, should fare much better in 2023 and beyond, compared to 2022. As a result, we are cautiously optimistic about improving our results. However, it is difficult to foresee what the impact will be on our businesses from inflation and rising interest rates, the on-going supply chain difficulties and associated delays, and the fear of a possible global recession. Further, while much less of an issue today, COVID-19 does remain a factor, particularly with respect to our Asian suppliers.”

Mr. Horowitz added “Furthermore, as was previously announced, our Board of Directors decided to reinstate the Company’s quarterly $0.05 per common share dividend. The Board believes this decision is appropriate at this time based upon the Company’s current financial condition, results of operations, capital requirements and other factors. Lastly, I am pleased to announce that the Company’s credit facility, which was set to expire in February 2024, was extended by an additional three years through February 2027. This amendment does not change any of the material terms, including the rates and fees charged, however we did agree to eliminate the capital expenditure line of $1.6 million, which we believe will not hinder our current growth plans.”

RESULTS OF OPERATIONS

2022 compared to 2021

REVENUE

The tables set forth below provide an analysis of our revenue for the years ended December 31, 2022, and 2021.

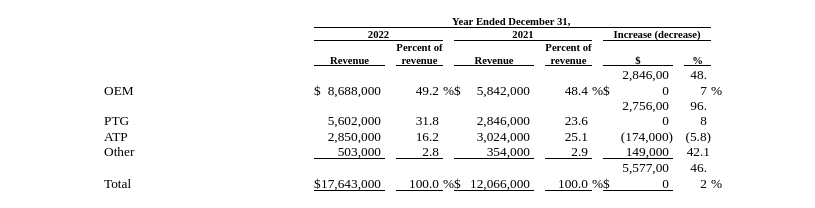

Consolidated

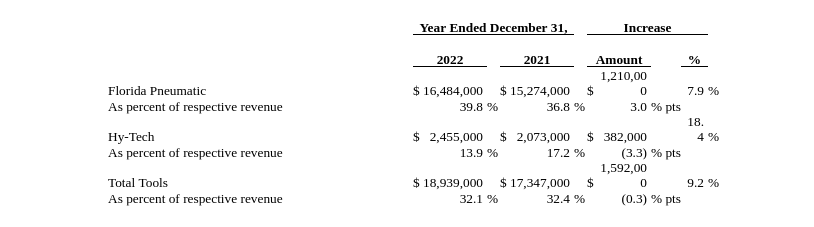

Florida Pneumatic

Florida Pneumatic markets its air tool products to four primary sectors within the pneumatic tool market; Automotive, Retail, Aerospace, and Industrial. It also generates revenue from its Berkley products line, as well as a line of air filters and other OEM parts (“Other”).

Florida Pneumatic’s full year 2022 revenue is slightly less ($90,000) than the prior year. Its 2022 Retail revenue declined 10.5%, when comparing the fiscal 2022 to the prior year. This decline was driven by several factors, including: a) sluggishness in consumer demand at The Home Depot (“THD”), most notably occurring during the fourth quarter of 2022, which we believe was due to rising interest rates and the general economy softness; b) lower sales of certain tools that enjoyed higher than usual volume during 2021, such as spray guns, which are used to combat the COVID-19 virus, and c) an effort by THD to lower its own inventory levels. 2022 Automotive revenue also declined when compared to 2021. The primary factors for the 5.8% reduction, were weak consumer demand occurring in the United States and, to a lesser extent, in Europe. Further, we believe this weakness in demand for our AIRCAT line of automotive products similar to the decline in Retail revenue, was driven by global rising interest rates and slowing economies. Both the above product lines are affected by the consumer market. Partially offsetting the above declines was a 20.5% increase in Florida Pneumatics’ higher gross margin, Jiffy product line. The key factor driving this increase throughout the year was stronger demand in 2022 from both the commercial and military sectors. Most of the Aerospace revenue is attributable to Jiffy Air Tool. Lastly, Florida Pneumatic’s Industrial revenue continued its growth during 2022 that commenced in the latter half of 2021. Its 2022 revenue increased 12.6% over 2021, which increased 51.9% over 2020. The primary factors driving this growth are an improved supply chain and increased demand in the foundry, metal fabrication, manufacturing, and assembly sectors.

Hy-Tech

Hy-Tech designs, manufactures, and sells a wide range of industrial products which are categorized as ATP for reporting purposes. In addition to Engineered Solutions, products and components manufactured for other companies under their brands are included in the OEM category in the table below. PTG revenue is comprised of products manufactured and sold by Hy-Tech’s gear business. NUMATX, Thaxton and other peripheral product lines, such as general machining, are reported as Other.

A key factor driving the 46.2% increase in Hy-Tech’s fiscal 2022 revenue, compared to the prior year was the acquisition of JGC that occurred in January 2022, which significantly contributed to the PTG revenue improvement of 96.8%, or more than $2,750,000. Additionally, Hy-Tech’s OEM revenue increased 48.7% over the prior year. This improvement is due primarily to increased shipments to a major OEM customer, and to a lesser extent, improved general market conditions in 2022, compared to 2021 during which Hy-Tech was impacted by the slowdown caused by the COVID global pandemic. The gross profit generated from the shipments to this OEM customer is less than historical OEM gross profit. The key factor for the increase in Hy-Tech’s Other revenue was a large one-time order for its Thaxton products. The decline (5.8%) in ATP revenue was driven by two factors; first, Hy-Tech’s ATP products continue to be price-challenged by off-shore suppliers, and second, the Company’s decision in 2021 to focus more of its design and marketing efforts on its OEM suite of products.

GROSS MARGIN

Florida Pneumatic’s Aerospace revenue generates stronger margins than its other product lines. Aerospace revenue increased as a percentage of Florida Pneumatic’s revenue, which in turn was a major factor in the improved gross margin. The vast majority of Florida Pneumatic’s Aerospace revenue is generated through the sale of the JIFFY product line. Additionally, other factors that contributed to Florida Pneumatic’s 300 basis point improvement were, its ability during fiscal 2022 to pass through some of the increases it incurred in ocean and domestic freight costs, as well as favorable foreign exchange rates, mostly related to the Taiwanese dollar. It should be noted that Florida Pneumatic’s ocean freight costs, particularly during the second half of 2021 through mid-2022 increased approximately five-fold, when compared to pre-pandemic rates. Our ocean freight costs have declined somewhat during the second half of 2022, but still remain above pre-pandemic levels. These improvements to gross margin were partially offset by increased warranty costs related to The Home Depot. Warranty costs lag in relation to shipments. As such, we believe these costs will decline over time.

Hy-Tech manufactures most of its products. Its gross margin is significantly affected by customer/product mix. Specifically, its largest OEM customers generates lower than average gross margin. We are continuing to increase prices and reduce manufacturing costs without jeopardizing the relationship with this major customer. Additionally, factors such as absorption of manufacturing overhead, raw material pricing, third-party costs, and the supply chain issues have affected its overall gross margin. Specifically, during 2022, Hy-Tech has encountered higher raw material, freight, and outside third-party vendor costs, all adversely affecting its gross margin in 2022. Further, during the latter portion of 2022 as Hy-Tech realigned its marketing and sales strategy, it determined that certain customers and products would no longer be serviced. As a result, Hy-Tech incurred an excess charge relating to obsolete, slow-moving inventory (“OSMI”). Further, Hy-Tech’s total gross margin was impacted by weak overhead absorption at its Punxsutawney, PA. facility, due primarily to integration issues of the Jackson Gear Company acquisition that occurred during the first quarter of 2022. We believe these issues will be corrected by the end of the second quarter of 2023.

SELLING, GENERAL AND ADMINISTRATIVE EXPENSES

Selling, general and administrative expenses (“SG&A”) include salaries and related costs, commissions, travel, administrative facilities, communications costs and promotional expenses for our direct sales and marketing staff, administrative and executive salaries, and related benefits, legal, accounting, and other professional fees as well as general corporate overhead and certain engineering expenses.

Our SG&A expenses during 2022 were $20,373,000, compared to $19,856,000, in 2021. Significant factors that contributed to the net change include:

-

i) Compensation expenses increased $676,000. Compensation expense is comprised of base salaries and wages, accrued performance-based bonus incentives and associated payroll taxes and employee benefits. Several factors contributed to this increase, among them the staffing added in connection with the JGC acquisition, increased wages primarily related to retention incentives and annual wage adjustments and increases in company-wide bonus/incentive/performance accruals.

ii) Professional fees and expenses increased $305,000, due primarily to legal, accounting, and other fees incurred in connection with the JGC acquisition. Other expenses that contributed to the increase in professional fees included ongoing cyber security/prevention costs, recruitment fees and legal fees associated with regulatory initiatives.

iii) Bad debt expense increased $96,000, when comparing 2022 to 2021. During the fourth quarter of 2022 we made several attempts to resolve and collect past due invoices from one customer, to no avail. It is extremely unlikely that we will be able to collect from this customer.

iv) Our depreciation and amortization increased $94,000 as the result of additional equipment purchased throughout the year and equipment and intangible assets acquired in connection with the Jackson Gear Company acquisition.

v) Temporary labor and stock-based compensation expense increased $35,000 and $36,000, respectively.

vi) Our variable expenses decreased $499,000. Driving this decline were significantly lower advertising costs at Florida Pneumatic, caused by a change in a distribution channel strategy.

vii) Our computer-related expenses declined $280,000. During the second quarter of 2021, we incurred approximately $288,000 in costs related to the May 2021 ransomware attack at our Florida Pneumatic subsidiary, where no such costs were incurred during 2022.

IMPAIRMENT OF ASSETS

During 2022 and 2021, we reduced by $48,000 and $88,000, respectively, the carrying value of certain not-in-use fixed assets to their fair value.

OTHER INCOME

In accordance with current accounting guidance, we recorded a gain of $19,000 during the fourth quarter of 2022 related to the early termination of a real property lease.

In December 2021 we completed the process of determining and verifying our eligibility and amount of payroll tax credits known as the Employee Retention Credit (“ERC”). This resulted in filing certain amended payroll tax forms, which, in the aggregate, totaled $2,028,000 of payroll tax credits. During 2022, we received approximately $112,000 of the ERC. In January 2023, we received approximately $1,677,000 of the ERC. The ERC is subject to federal and local tax. Pursuant to the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”), on April 20, 2020, we received a Paycheck Protection Program (“PPP”) loan, in the amount of $2,929,000. Under the terms of the CARES Act, as amended, we were eligible to apply for forgiveness for all or a portion of the PPP loan. In February 2021, we filed an application for forgiveness with the lender, who approved this submission and submitted the application for forgiveness to the Small Business Administration. On June 9, 2021, we were advised that the SBA had approved our PPP loan forgiveness application. Accordingly, the lender applied the funds it received from the SBA and paid off PPP loan principal and interest in full. In accordance with accounting guidance this forgiveness of debt and related accrued interest was be accounted for as Other Income and Interest Expense – Net, in 2021, and was not considered as taxable income.

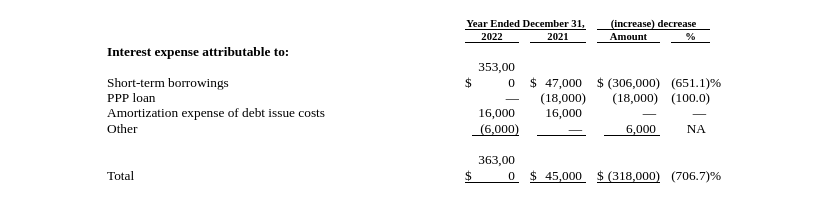

INTEREST EXPENSE - NET

The most significant factor causing the increase in our short-term borrowings interest expense was the growth in the prime rate during 2022. The Applicable Margin, as defined in our Credit Agreement during fiscal 2022 ranged from 1.5% to 2.10% applied to LIBOR /SOFR borrowings and from 0.50% to 1.60% applied to Base rate borrowings. The interest charged on Base rate borrowings, (effectively borrowings at Prime rate) before adding Applicable Margin increased from 3.25% in January 2022 to 7.50% at December 31, 2022. Further, the interest rate before the Applicable Margin for LIBOR / SOFR term borrowings increased from an average of 1.61% in January 2022 to an average of 6.20% for borrowing in December 2022. Our average monthly borrowings under the Credit Facility during fiscal 2022 ranged from $7,852,000 to $12,654,000. The average monthly short-term borrowing during fiscal 2022 was $9,845,000, compared to $2,686,000 during the prior year. The increase was driven by the Jackson Gear Company business acquisition in January 2022. Additional working capital needs are due to the anticipated growth, and a roll-out of a tools program to our retail customer. Our Revolver borrowings increased significantly in the first half of 2022 and began to decline during the second half of 2022. At December 31, 2022 our borrowing under the Credit Facility was net $7,570,000. (See Liquidity and Capital Resources for further discussion).

The amortization expense is related to the debt issue costs associated with amendments to our banking facility.

Lastly, Other relates to interest income in connection with Tax refunds received in fiscal 2022.

INCOME TAX EXPENSE

The benefit from income taxes was $376,000 in 2022, compared to $2,000 in 2021. Significant factors impacting the 2022 net effective tax benefit rate were non-deductible permanent differences, and state and local taxes. The net effective tax benefit for 2022 was (20.3%).

LIQUIDITY AND CAPITAL RESOURCES

We monitor such metrics as days? sales outstanding, inventory requirements, inventory turns, estimated future purchasing requirements and capital expenditures to project liquidity needs, as well as evaluate return on assets. Our primary sources of funds are operating cash flows, existing working capital and our Revolver Loan (?Revolver?) with our Bank.

We gauge our liquidity and financial stability by various measurements, some of which are shown in the following table:

Credit facility

Currently our Credit Facility, will be discussed in detail in the Company’s Form 10-K. This Credit Facility was amended in March 2023. Key components of the current amendment include extending the expiration date to February 8, 2027, and the removal of the $1,600,000 CapEx facility.

Additionally, should the need arise whereby the current Credit Facility is insufficient; we could obtain additional funds based on the value of our real property.

Cash flows

For the year ended December 31, 2022, cash provided by operating activities was $3,288,000, compared to cash used in operating activities for the year ended December 31, 2021, of $4,149,000. At December 31, 2022, our consolidated cash balance was $667,000, compared to $539,000 at December 31, 2021. Cash at our UAT subsidiary on December 31, 2022, and 2021 was $49,500 and $190,000, respectively. We operate under the terms and conditions of the Credit Agreement. As a result, all domestic cash receipts are remitted to Capital One lockboxes.

Capital spending during the year ended December 31, 2022, was $2,374,000, compared to $642,000 in 2021. Capital expenditures currently planned for 2023 are approximately $2,600,000 which we expect will be financed through the Credit Facility. The major portion of these planned capital expenditures will be for new metal cutting equipment, tooling and information technology hardware and software.

Our liquidity and capital is primarily sourced from our credit facility, and cash provided by operations. At December 31, 2022, we had $7,678,000 available to us from the revolver portion of the credit facility.

For the year ended December 31, 2022, we had $7,235,000 of open purchase order commitments, compared to $16,331,000 at December 31, 2021.

ABOUT P&F INDUSTRIES, INC.

P&F Industries, Inc., through its wholly owned subsidiaries, is a manufacturer and importer of air-powered tools and accessories sold principally to the aerospace, industrial, automotive, and retail markets. P&F?s products are sold under its own trademarks, as well as under the private labels of major manufacturers and retailers.

For information relating to the products and services we offer, please visit our website at www.pfina.com. From there you can link to our subsidiary websites.

OTHER INFORMATION

P&F Industries Inc. has scheduled a conference call on March 28, 2023, at 11:00 A.M. Eastern Time, to discuss its full year 2022 results and financial condition. Investors and other interested parties who wish to listen to or participate can dial 1-866-580-3963. It is suggested you call at least 10 minutes prior to the call commencement. For those who cannot listen to the live broadcast, a replay of the call will also be available on the Company’s website beginning on or about March 29, 2023.

Forward Looking Statement

The Private Securities Litigation Reform Act of 1995 (the ?Reform Act?) provides a safe harbor for forward-looking statements made by or on behalf of P&F Industries, Inc., and subsidiaries (?P&F?, or the ?Company?). P&F and its representatives may, from time-to-time, make written or verbal forward-looking statements, including statements contained in the Company?s filings with the Securities and Exchange Commission and in its reports to shareholders. Generally, the inclusion of the words ?believe,? ?expect,? ?intend,? ?estimate,? ?anticipate,? ?will,? ?may,? ?would,? ?could,? ?should,? and their opposites and similar expressions identify statements that constitute ?forward-looking statements? within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 and that are intended to come within the safe harbor protection provided by those sections. Any forward-looking statements contained herein, including those related to the Company?s future performance, are based upon the Company?s historical performance and on current plans, estimates and expectations. All forward-looking statements involve risks and uncertainties. These risks and uncertainties could cause the Company?s actual results for all or part the 2022 fiscal year and beyond to differ materially from those expressed in any forward-looking statement made by or on behalf of the Company for a number of reasons including, but not limited to:

- Risks related to the global outbreak of COVID-19 and other public health crises;

- Risks associated with sourcing from overseas;

- Disruption in the global capital and credit markets;

- Importation delays;

- Customer concentration;

- Unforeseen inventory adjustments or changes in purchasing patterns;

- Market acceptance of products;

- Competition;

- Price reductions;

- Exposure to fluctuations in energy prices;

- Exposure to fluctuations within the cost of raw materials;

- The strength of the retail economy in the United States and abroad;

- Adverse changes in currency exchange rates;

- Interest rates;

- Debt and debt service requirements;

- Borrowing and compliance with covenants under our credit facility;

- Impairment of long-lived assets and goodwill;

- Retention of key personnel;

- Acquisition of businesses;

- Regulatory environment;

- Litigation and insurance;

- The threat of terrorism and related political instability and economic uncertainty; and

and those other risks and uncertainties described in its Annual Report on Form 10-K for the year ended December 31, 2021 (?2021 Form 10-K?), its Quarterly Reports on Form 10-Q, and its other reports and statements filed by the Company with the Securities and Exchange Commission. Forward-looking statements speak only as of the date on which they are made. The Company undertakes no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future developments or otherwise. The Company cautions you against relying on any of these forward-looking statements.

CONSOLIDATED BALANCE SHEET (PDF)

P&F Industires, Inc. make available forms & documents which are available for download. These forms & documents are in Adobe® PDF (portable document file) format. In order to view these forms & documents, you must have Adobe® Acrobat® 7 Reader. If you don't have the reader, you can download it for free from Adobe® by clicking here or on the "Get Acrobat® Reader" icon below.

![]()