News

2023 Press releases

P&F Industries, Inc.

Joseph A. Molino, Jr.

Chief Operating Officer

631-694-9800

www.pfina.com

Joseph A. Molino, Jr.

Chief Operating Officer

631-694-9800

www.pfina.com

P&F INDUSTRIES, INC. REPORTS IMPROVED RESULTS FOR THE THREE-MONTH PERIOD ENDED MARCH 31, 2023

MELVILLE, N.Y., May 11, 2023 - P&F Industries, Inc. (NASDAQ: PFIN) today

announced its results from operations for the three-month period ended March 31, 2023. The

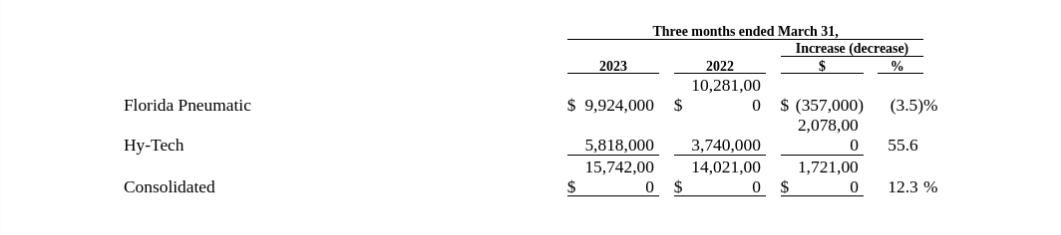

Company is reporting net revenue for the three-month period ended March 31, 2023, of $15,742,000,

compared to $14,021,000 for the same three-month period in 2022. Additionally, the Company is

reporting a net income before income taxes of $494,000 for the three-month period ended March 31,

2023, compared to a net loss before income taxes of $714,000, for the three-month period ended March

31, 2022. The Company is reporting a net income after-taxes of $337,000 for the three-month period

ended March 31, 2023, compared to a net loss after-taxes of $618,000 for the same three-month period a year ago.

Lastly, the Company stated that its basic and diluted income per share for the three-month period ended March 31,

2023, was $0.11, compared to a basic and diluted loss per share of $0.19 for the same three-month period a year ago.

Richard Horowitz, the Company’s Chairman of the Board, Chief Executive Officer and President commented, “I am very pleased to report that, when comparing the three-month periods ended March 31, 2023, and 2022, our revenue increased $1,721,000 and our income before taxes improved by $1,208,000. Revenue at Hy-Tech increased 55.6% or almost $2.1 million. Our PTG product line had the most significant improvement, percentage-wise, with revenue increasing 105.6% this quarter, compared to the same three-month period in 2022. Our OEM product line had the largest dollar revenue growth with sales up by more than $1.1 million compared to the same three-month period in 2022. Although Florida Pneumatic’s revenue this quarter declined 3.5% from the same period last year, due to weakness in its Automotive and Retail product lines, its higher margin Aerospace revenue improved 35.7%, which led to its increased gross margin and gross profit.”

Mr. Horowitz continued, “Our first quarter 2023 consolidated gross margin was 36.5%, compared to 32.2% for the same period a year ago. This improvement was driven primarily by price increases that began in mid to late 2022, lower ocean freight costs, improved absorption of manufacturing overhead and product mix. Additionally, the early-stage start-up issues related to the integration of the Jackson Gear acquisition have significantly decreased.

Despite the 12.3% increase in net revenue, we were able to control our total operating expenses, which increased only $2,000. It should be noted that during the first quarter of 2022 we incurred approximately $150,000 of acquisition-related expenses pertaining to the Jackson Gear Company business acquisition, which was included in our selling, general and administrative expenses.”

Mr. Horowitz concluded “We are doing our best to navigate through these challenging times caused by rising inflation, an unsettled U.S. economy, and ongoing global supply chain issues. We believe that P&F should continue to see improved results, as customer orders are strong, costs and expenses are less volatile than in the recent past, and manufacturing overhead absorption continues to improve. In addition, there are multiple growth opportunities provided by both the Jackson Gear business acquisition and our other product lines.”

The Company will be reporting the following.

TRENDS AND UNCERTAINTIES

INTERNATIONAL SUPPLY CHAIN

Although much less than during the first quarter of 2022, we continue to encounter delays in receiving inventory from our Asian suppliers, which leads to intermittent shortages of inventory. Our ocean freight costs, which had increased significantly during the COVID-19 pandemic, have recently returned to pre-pandemic levels. The above factors continued in the first quarter of 2023 to impact our results. Lastly, we believe the following international supply chain issues have also negatively impacted our 2023 results:

- Increased price of fuel;

- Shortage of shipping containers;

- Congestion at the ports in Asia and the United States.

At the present time, we believe that some or all of the above-mentioned supply chain disruptions will likely continue for some time in fiscal 2023. While we believe that most of the related costs associated with the issues discussed above have been factored into our selling price, there is no assurance that we will be able to pass through any future additional direct costs or costs incurred related to our international supply chain issues in the future.

DOMESTIC TRANSPORTATION COSTS

During the first quarter of 2023 supply chain conditions continued to improve yielding lower domestic transportation costs. The availability of port to warehouse transportation services has improved significantly compared to 2022 and associated domestic freight rates have continued to moderate although rising fuel costs (diesel) have tempered rate reductions.

IMPACT OF INFLATION/GEOPOLITICAL ISSUES

We believe that the current and projected levels of inflation, as well as a possible economic recession will likely continue to have an effect on our manufacturing and operating costs. At the present time, we are unable to reasonably estimate the impact inflation and geo-political issues will have on our results of operations for the foreseeable future.

We believe that our results of operations and financial condition during 2023, were not materially impacted by the Russia-Ukraine conflict, however we cannot predict what impact this conflict may have on our results in the future.

BOEING

Sales of aircraft by Boeing have been depressed since the two 737 MAX crashes in 2018 and 2019. Further, the Federal Aviation Administration grounded all 737 MAX aircraft for several quarters. These events, coupled with the COVID-19 pandemic reduced Boeing’s aircraft production levels to well below those prior to the pandemic and the grounding. In 2019, Boeing produced 52 737 MAX aircraft per month. It is currently still producing significantly below that level. Per Boeing, it plans to return to those levels in 2025 and expects to add a fourth 737 MAX production line in 2024. We believe that these stated plans along with the return of the Boeing 787 aircraft, which has also had production delays to full production, will be beneficial to P&F’s aerospace sales in the next several years.

TECHNOLOGIES

We believe that over time, several newer technologies and features will have a greater effect on the market for our traditional pneumatic tool offerings. So far, the greatest impact has been on the automotive aftermarket with the advent of advanced cordless operated tools. Currently, we do not offer a cordless tool to the automotive aftermarket. However, with respect to the industrial market, we have developed for one of our largest OEM customers a tool mechanism that is incorporated into a major line of their cordless power tools. These tools have been in full production with our supplied system for several years and our sales of these products have continued to grow over that time. We continue to analyze the practicality of developing or incorporating newer technologies in our tool platforms for other markets as well. This includes adding our internally developed mechanisms to existing cordless power sources as well as producing complete cordless tool systems. In addition, we have recently developed a cordless installation tool for the aerospace market. We have begun taking orders for this product and we expect to introduce other versions later in 2023.

OTHER MATTERS

Other than the trends and uncertainties mentioned above, or matters that may be discussed below, there are no major trends or uncertainties that had, or we could reasonably expect to have a material impact on our revenue and operations, nor was there any unusual or infrequent event, transaction or any significant economic change that materially affected our results of operations.

RESULTS OF OPERATIONS

REVENUE

The tables below provide an analysis of our net revenue for the three-month periods ended March 31, 2023, and 2022:

Consolidated

Florida Pneumatic

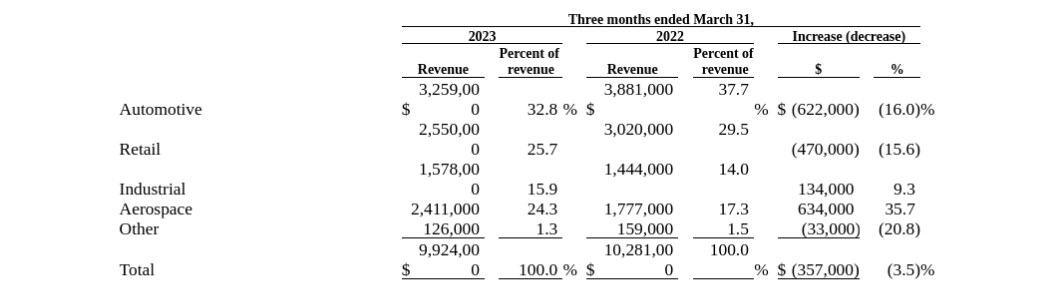

Florida Pneumatic markets its air tool products to four primary sectors within the pneumatic tool market; Automotive, Retail, Aerospace and Industrial. It also generates revenue from its Berkley products line, as well as a line of air filters and other OEM parts (“Other”).

Automotive revenue declined this quarter, compared to the same period in 2022, due primarily to an across-the-board price increase in all distribution channels in order to address rising input costs. This change in pricing strategy led to a decline in number of unit sales and thus overall revenue in this category. However, Automotive gross margin improved as a result of this change. The primary factors contributing to the 15.6% decline in our Retail revenue were: a) a decision by The Home Depot (“THD”) to reduce in-store inventory levels; b) a reduction in display area at THD stores; c) a net reduction in the number of items being offered by THD this quarter, compared to the same three-month period in 2022, and d) increased pressure from on-line distributors, as well as and other “brick and mortar” retailers expanding their presence in this product line. Partially offsetting the above-mentioned declines our Aerospace revenue improved 35.7% when comparing the first quarter of 2023 and 2022. This improvement was driven by, among other factors, increased demand for new, limited life parts that JIFFY has begun to market, and an overall increase in demand throughout the sector for standard drilling, installation and torque control tools. Lastly, our Industrial revenue increased primarily due to improved general market conditions.

Hy-Tech

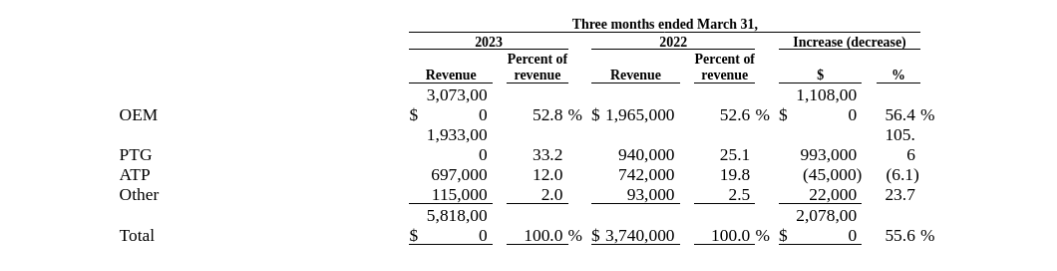

Hy-Tech designs, manufactures, and sells a wide range of industrial products which are categorized as ATP for reporting purposes. In addition to Engineered Solutions, products and components manufactured for other companies under their brands are included in the OEM category in the table below. PTG revenue is comprised of products manufactured and sold by Hy-Tech’s gear business. NUMATX, Thaxton and other peripheral product lines, such as general machining, are reported as Other.

The $1.1 million increase in OEM revenue this quarter, compared to the first quarter of 2022, was driven by growth in certain markets that are served by a number of Hy-Tech’s OEM customers. The markets served by our customers include multiple industrial applications, as well as the tool rental market. PTG revenue for the first three months of 2023 more than doubled its revenue reported for the same period a year ago. This improvement was driven by the acquisition of the Jackson Gear Company business that we acquired in January 2022. The increase in Hy-Tech’s Other revenue was due to stronger NUMATX and general machining revenue growth this quarter, compared to the same three-month period in 2022. The modest decline in ATP revenue is attributable to our decision to focus our marketing efforts on OEM and PTG product offerings.

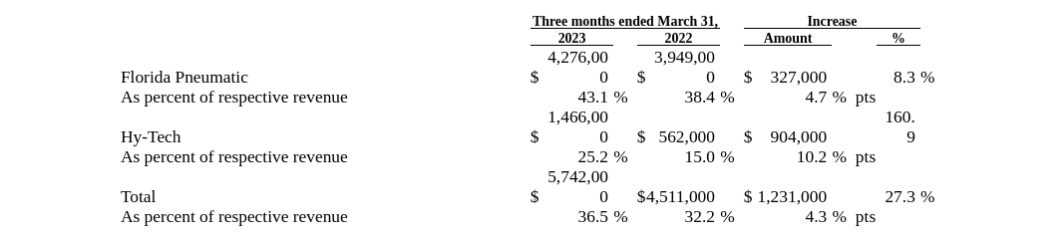

GROSS MARGIN/PROFIT

During the first quarter of 2023, Florida Pneumatic’s gross margin improved compared to the same period in the prior year principally due to a shift away from the lower margin product lines, Retail and Automotive, to the higher margin, industrial and aerospace categories. Additionally, during 2022, we raised prices in all product categories.

The improvement in Hy-Tech’s gross margin is due primarily to its overall product/customer mix. Additionally, cost and expense reductions, coupled with revisions in pricing structure, enabled Hy-Tech to improve its blended gross margin, thus contributing to the overall gross margin improvement. We continue to focus on improving manufacturing overhead absorption, particularly at our PTG facility. While always ongoing, we expect the process of integrating the Jackson Gear Company acquisition to be effectively complete by approximately mid-2023.

SELLING, GENERAL AND ADMINISTRATIVE EXPENSES

Selling, general and administrative expenses (“SG&A”) include salaries and related costs, commissions, travel, administrative facilities costs, communications costs and promotional expenses for our direct sales and marketing staff, administrative and executive salaries and related benefits, legal, accounting, and other professional fees as well as general corporate overhead and certain engineering expenses.

During the first quarter of 2023, our SG&A was $5,175,000, compared to $5,173,000, incurred during the same three-month period in 2022. Significant components to the net change include: a) compensation expenses increased $223,000, due to several factors, among them the additional staffing added throughout the Company, increased wages primarily related to retention incentives and annual wage adjustments and increases in company-wide bonus/incentive/performance accruals; b) increased depreciation and amortization of $51,000; c) professional fees and expenses decreased $140,000, due primary to legal, accounting and other fees incurred in connection with the JGC acquisition during the first quarter of 2023 not recurring in the first quarter of 2023; and d) variable expenses declined $131,000. Variable expenses include among other items, commissions, freight out, travel, advertising, shipping supplies and warranty costs. Driving this decline was lower advertising and shipping costs at Florida Pneumatic, caused primarily by lower Retail revenue this quarter and a reduction in discretionary Automotive advertising expenses, compared to the same period a year ago.

OTHER INCOME

During the three-month period ended March 31, 2023, we recognized a gain of $21,000 from the sale of fully depreciated equipment. Additionally, as a result of final resolution of our Employee Retention Tax Credit (“ERTC”) filing, we recorded an additional $15,000 as Other Income. This income is subject to federal and local tax.

INTEREST – NET

The most significant factor causing the increase in our short-term borrowings interest expense was the growth in the SOFR and prime rates. Most of our borrowings are SOFR plus Applicable Margin. The Applicable Margin, as defined in our Credit Agreement, during the three-month period ended March 31, 2023, was 2.10% applied to all SOFR borrowings and 1.60% applied to Base Rate borrowings. The Applicable Margin that was added to LIBOR and Base Rate borrowings during the three-month period ended March 31, 2022, were 1.50% and 0.50%, respectively. During the three-month period ended March 31, 2023, the SOFR rates ranged from 4.43% to 4.86%, compared to LIBOR rates, which we were using during the first quarter of 2022, that ranged from 0.10% to 0.47%. Further, the prime rate, which is the interest rate used for Base Rate borrowings before the Applicable Margin, during the first three months of 2023 ranged from 7.5% to 8.0%, compared to prime rates ranging from 3.25% to 3.50% during the same three-month period in 2022.

The amortization expense incurred during the three-month period ended March 31, 2023, is related to the debt issue costs associated with Amendment 11 to our banking facility

The average balance of short-term borrowings during the three-month periods ended March 31, 2023, and 2022, were $7,287,000, and $10,157,000, respectively.

INCOME TAXES

At the end of each interim reporting period, we compute an effective tax rate based upon our estimated full year results. This estimate is used to determine the income tax provision or benefit on a year-to-date basis and may change in subsequent interim periods. Accordingly, the effective tax rate for the three-month periods ended March 31, 2023, and 2022, were approximately a tax provision rate of 31.8% and tax benefit rate 13.4%, respectively. The effective tax rates for all periods presented were impacted primarily by state taxes, and non-deductible expenses.

LIQUIDITY AND CAPITAL RESOURCES

We monitor such metrics as days’ sales outstanding, inventory requirements, inventory turns, estimated future purchasing requirements and capital expenditures to project liquidity needs, as well as evaluate return on assets. Our primary sources of funds are operating cash flows, existing working capital and our Revolver Loan (“Revolver”) with our Bank.

We gauge our liquidity and financial stability by various measurements, some of which are shown in the following table:

Credit facility

We and Capital One Bank, NA entered into an amendment to the Credit Facility that, among other things, extended the expiration date to February 8, 2027.

At March 31, 2023, there was approximately $7,800,000 available to us under the Revolver arrangement.

Cash flows

For the three-month period ended March 31, 2023, cash provided by operating activities was $790,000, compared to cash used by operating activities for the three-month period ended March 31, 2022, of $3,972,000. At March 31, 2023, and 2022, our consolidated cash balance was $561,000, and $642,000, respectively. We operate under the terms and conditions of the Credit Agreement. As a result, all domestic cash receipts are remitted to Capital One lockboxes. Thus, nearly all cash on hand represents funds to cover checks issued but not yet presented for payment.

Our total debt to total book capitalization (total debt divided by total debt plus equity) at both March 31, 2023, and December 31, 2022, was 15.3%.

During the three-month period ended March 31, 2023, we used $905,000 for capital expenditures, compared to $380,000 during the same period in the prior year. Capital expenditures currently planned for the remainder of 2023 are approximately $2,400,000, which we expect will be financed through the Credit Facility.

The major portion of these planned capital expenditures will be for new metal cutting equipment, tooling and information technology hardware and software.

The major portion of these planned capital expenditures will be for new metal cutting equipment, tooling and information technology hardware and software.

Our liquidity and capital are primarily sourced from our Credit Facility.

Should the need arise whereby the current Credit Agreement is insufficient, we could obtain additional funds based on the value of our real property, and we believe the borrowing under the current Agreement could be increased.

IMPACT OF INFLATION

During the three-month period ended March 31, 2023, with respect to our cost of inventory, we encountered price increases in raw materials, imported parts and tools, ocean freight and labor. Additionally, our operating costs continue to encounter cost/price increases. It is difficult to accurately determine what portion of the above referenced increases are attributable to inflation. We have been able to pass through most of the above-mentioned price increases, however we cannot predict our ability to continue this practice, nor to what degree. We intend to continue to actively manage the impact of inflation on our results of operations, however, we cannot reasonably estimate possible future impacts at this time.

ABOUT P&F INDUSTRIES, INC.

P&F Industries, Inc., through its wholly owned subsidiaries, is a leading manufacturer and importer of air-powered tools and accessories sold principally to the aerospace, industrial, automotive, and retail markets. P&F’s products are sold under its own trademarks, as well as under the private labels of major manufacturers and retailers.

For information relating to the products and services we offer, please visit our website at www.pfina.com From there you can link to our subsidiary websites.

OTHER INFORMATION

P&F Industries Inc. has scheduled a conference call on May 11, 2023, at 11:00 A.M. Eastern Time, to discuss its first quarter 2023 results and financial condition. Investors and other interested parties who wish to listen to or participate can dial 1-866-580-3963. It is suggested you call at least 10 minutes prior to the call commencement. For those who cannot listen to the live broadcast, a replay of the call will also be available on the Company’s website beginning on or about May 12, 2023.

Forward Looking Statement

The Private Securities Litigation Reform Act of 1995 (the “Reform Act”) provides a safe harbor for forward-looking statements made by or on behalf of P&F Industries, Inc., and subsidiaries (“P&F”, or the “Company”). P&F and its representatives may, from time-to-time, make written or verbal forward-looking statements, including statements contained in the Company’s filings with the Securities and Exchange Commission and in its reports to shareholders. Generally, the inclusion of the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “will,” “may,” “would,” “could,” “should,” and their opposites and similar expressions identify statements that constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 and that are intended to come within the safe harbor protection provided by those sections. Any forward-looking statements contained herein, including those related to the Company’s future performance, are based upon the Company’s historical performance and on current plans, estimates and expectations. All forward-looking statements involve risks and uncertainties. These risks and uncertainties could cause the Company’s actual results for all or part the 2022 fiscal year and beyond to differ materially from those expressed in any forward-looking statement made by or on behalf of the Company for a number of reasons including, but not limited to:

- Risks related to the global outbreak of COVID-19 and other public health crises;

- Risks associated with sourcing from overseas;

- Disruption in the global capital and credit markets;

- Importation delays;

- Customer concentration;

- Unforeseen inventory adjustments or changes in purchasing patterns;

- Market acceptance of products;

- Competition;

- Price reductions;

- Exposure to fluctuations in energy prices;

- Exposure to fluctuations within the cost of raw materials;

- The strength of the retail economy in the United States and abroad;

- Adverse changes in currency exchange rates;

- Interest rates;

- Debt and debt service requirements;

- Borrowing and compliance with covenants under our credit facility;

- Impairment of long-lived assets and goodwill;

- Retention of key personnel;

- Acquisition of businesses;

- Regulatory environment;

- Litigation and insurance;

- The threat of terrorism and related political instability and economic uncertainty; and

- Business disruptions or other costs associated with information technology, cyber-attacks, system implementations, data privacy or catastrophic losses,

and those other risks and uncertainties described in its Annual Report on Form 10-K for the year ended December 31, 2022 (“2022 Form 10-K”), its Quarterly Reports on Form 10-Q, and its other reports and statements filed by the Company with the Securities and Exchange Commission. Forward-looking statements speak only as of the date on which they are made. The Company undertakes no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future developments or otherwise. The Company cautions you against relying on any of these forward-looking statements.

CONSOLIDATED BALANCE SHEET (PDF)

P&F Industires, Inc. make available forms & documents which are available for download. These forms & documents are in Adobe® PDF (portable document file) format. In order to view these forms & documents, you must have Adobe® Acrobat® 7 Reader. If you don't have the reader, you can download it for free from Adobe® by clicking here or on the "Get Acrobat® Reader" icon below.

![]()